Blockchain is one of the core technologies behind cryptocurrency, but many beginners find it confusing.

You may hear people talk about Bitcoin, Ethereum, digital currencies, and distributed ledgers as if they mean the same thing. However, they are not the same.

Understanding this technology helps explain how cryptocurrencies can move online without banks or payment processors approving every transaction.

Fortunately, the basic idea is easier to understand than most people think.

If you’re completely new to digital assets, start with our Complete Beginner’s Guide to Cryptocurrency, which explains cryptocurrency, wallets, exchanges, and distributed ledger basics in one step-by-step resource.

In this beginner’s guide, you’ll learn:

- What blockchain is

- Why it was created

- How the process works step by step

- Why the technology offers strong security features

- The difference between Bitcoin and the system behind it

- Real-world uses beyond cryptocurrency

- Common beginner misconceptions

- The advantages and limitations to understand

By the end, you’ll have a practical understanding without needing a technical background.

Table of Contents

What Is Blockchain?

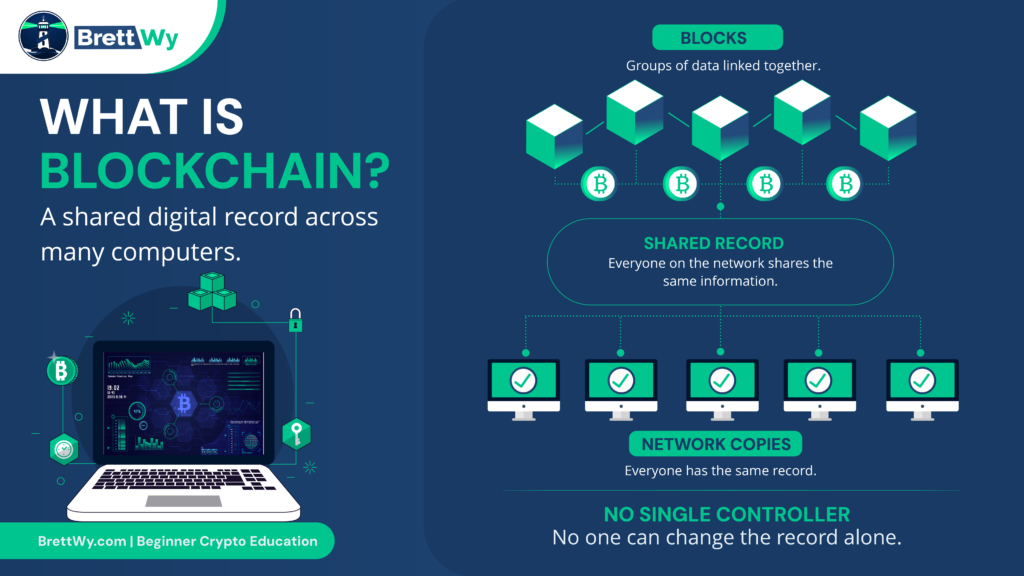

Blockchain is a shared digital record-keeping system that stores information across many computers instead of in one central location.

It records transactions and other data in groups called blocks. Then, each new block connects to the blocks before it, creating a continuous chain of records.

That linked structure explains the name.

A Simple Beginner Definition

Think of a community scoreboard in a town square.

Everyone can see the scoreboard. When the score changes, many people update their copies at the same time.

As a result, one person cannot easily change the score in secret.

A distributed ledger works in a similar way.

Instead of one company controlling the records, many computers maintain matching copies.

Why Blockchain Matters

Traditional digital systems usually place control in the hands of one organization, such as:

- A bank

- A government agency

- A social media company

- A payment processor

By contrast, a shared ledger allows many participants to maintain records together.

Because of that structure, the system can create:

- Greater transparency

- Reduced reliance on intermediaries

- Improved resilience

- New ways to transfer value online

Why Is It Called a Blockchain?

The system groups information into containers called blocks.

Each block includes a reference to the one before it.

Over time, these connected blocks form a chain.

Block + Chain = Blockchain

Why Was Blockchain Created?

Blockchain was created to solve a trust problem: how can strangers exchange value online without relying on a central authority?

Before Bitcoin, digital payments usually needed trusted intermediaries.

For example, common intermediaries include:

- Banks

- Credit card companies

- Payment processors

These organizations maintain records and verify transactions.

The Trust Problem

Imagine a school where students track points during the year.

If only one teacher keeps the scorebook, everyone must trust that teacher’s records.

However, if hundreds of students each maintain the same copy, everyone can verify the score independently.

That is the basic trust idea behind a distributed ledger.

The Double-Spending Problem

Digital files can usually be copied.

Therefore, if digital money could be copied like a photo, people could spend the same money repeatedly.

This challenge is called the double-spending problem.

A shared transaction history helps solve this issue because everyone can verify whether money has already moved.

The Bitcoin Connection

This technology first gained widespread attention through Bitcoin.

In 2008, Satoshi Nakamoto published a paper describing a decentralized digital money system.

Then, Bitcoin became the first successful major use of blockchain technology.

Readers interested in the original vision behind Bitcoin can review Satoshi Nakamoto’s Bitcoin white paper.

How Does Blockchain Work?

Blockchain works by recording transactions, verifying them through a network, grouping them into blocks, and permanently adding those blocks to a shared ledger.

Let’s follow a simple example.

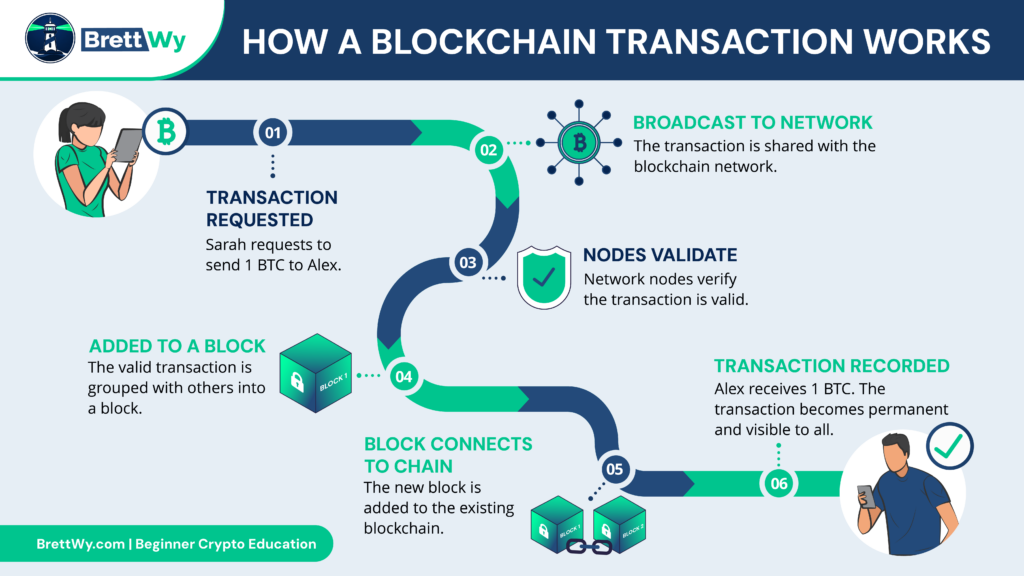

Imagine Sarah wants to send 1 Bitcoin to Alex.

Step 1: A Transaction Is Requested

Sarah starts a transaction.

The request includes:

- Sender information

- Recipient information

- Amount being transferred

Next, the transaction enters the network.

Step 2: The Transaction Is Broadcast

The network shares the transaction with participating computers.

These computers are called nodes.

What Are Nodes?

A node is a computer that participates in a blockchain network.

Nodes help:

- Store network data

- Verify transactions

- Maintain system integrity

In many public networks, thousands of nodes participate at the same time.

Step 3: The Network Validates the Transaction

Nodes check that:

- Sarah owns the Bitcoin

- The Bitcoin has not already moved elsewhere

- The transaction follows the rules

To do this, the system uses cryptography and consensus mechanisms.

What Is Cryptography?

Cryptography uses mathematics to secure information.

For example, it helps ensure:

- Transactions are authentic

- People cannot easily alter records

- The network can verify ownership

Because of this, cryptography forms one of the foundations of secure digital asset networks.

Step 4: The Transaction Enters a Block

After validation, the network groups transactions together.

This collection forms a block.

Depending on the network, one block may contain hundreds or thousands of transactions.

Step 5: The Block Is Connected to Previous Blocks

The new block receives a reference to the block before it.

As a result, the network creates a continuous historical record.

To change one block, someone would also need to change every connected block after it.

That is one reason historical records are difficult to alter.

Step 6: The Transaction Becomes Permanent

Finally, the network accepts the block and adds it to the chain.

The transaction now appears in the shared record.

Alex receives the Bitcoin.

Then, the shared ledger updates across participating nodes.

Now that you understand the basic process, the next step is learning how cryptocurrencies use these networks. Our guide on How Cryptocurrency Works walks through the entire process in beginner-friendly language.

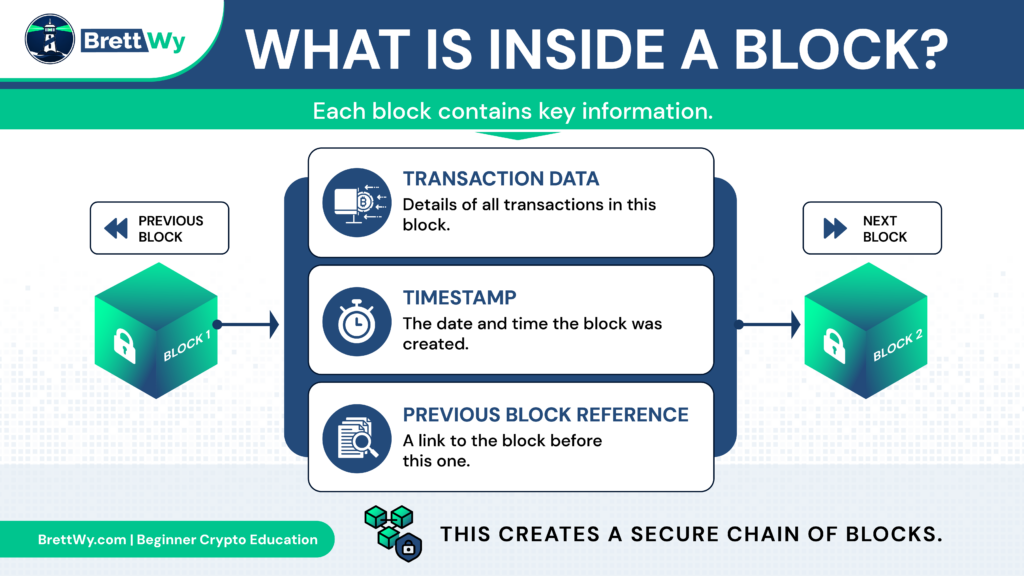

What Is a Block?

A block is a container that stores verified information before it joins the blockchain.

In simple terms, blocks are the building units of the chain.

What Information Does a Block Contain?

Most blocks contain:

- Transaction data

- A timestamp

- A reference to the previous block

Transaction Data

This records activity occurring on the network.

For example, it may include:

- Cryptocurrency transfers

- Smart contract activity

- Asset ownership changes

Timestamp

The timestamp shows when the network created the block.

Therefore, it helps establish the order of events.

Previous Block Reference

Each block references the block before it.

Because of this reference, the system forms a chain structure.

What Is a Blockchain Network?

A blockchain network is a group of connected computers that collectively maintain and verify shared records.

No single computer controls the entire system.

Instead, many participants share responsibility.

Distributed Ledger Explained

A distributed ledger is a shared database stored across many computers.

Each participant maintains a copy.

When updates happen, the network synchronizes those changes across participants.

As a result, this design can provide more resilience than a single-server system.

Why Distributed Systems Matter

If one computer fails:

- The network continues operating

- Records remain available

- The system does not lose the data

Therefore, distributed systems reduce single points of failure.

What Are Consensus Mechanisms?

Consensus mechanisms are systems that help network participants agree on which transactions are valid.

Without consensus, participants might disagree about transaction history.

Therefore, consensus keeps everyone synchronized.

Proof of Work

Proof of Work is the mechanism Bitcoin uses.

In this system, participants called miners compete to solve mathematical problems.

The winner earns the right to add a new block.

Who Are Miners?

Miners use computing power to validate transactions and secure certain networks.

In other words, they help maintain system integrity.

Proof of Stake

Proof of Stake selects participants based on cryptocurrency holdings committed to network security.

These participants are called validators.

Who Are Validators?

Validators help verify transactions and maintain security in Proof of Stake systems.

Many newer networks use this approach because it requires less energy than Proof of Work.

Why Consensus Matters

Consensus mechanisms help ensure:

- Accurate records

- Network security

- Agreement among participants

- Resistance to fraud

Why Is Blockchain Considered Secure?

Blockchain offers strong security features because it combines decentralization, cryptography, transparency, and tamper-resistant record keeping.

No system is perfectly secure. However, this design introduces several protective layers.

For a deeper technical overview of blockchain security concepts, review the NIST Blockchain Technology Overview.

Decentralization

Decentralization distributes control across many participants instead of concentrating it in one organization.

As a result, the system depends less on a central authority.

If one participant fails, the network can continue functioning.

Cryptography

Cryptography helps secure transactions and verify ownership.

For example, only authorized users can initiate transfers from their wallets.

Transparency

Many public networks allow anyone to inspect transaction records.

Because of that visibility, participants can verify activity independently.

Immutability

Immutability means records become extremely difficult to alter after confirmation.

To change historical records, an attacker would need to overcome major technical and economic barriers.

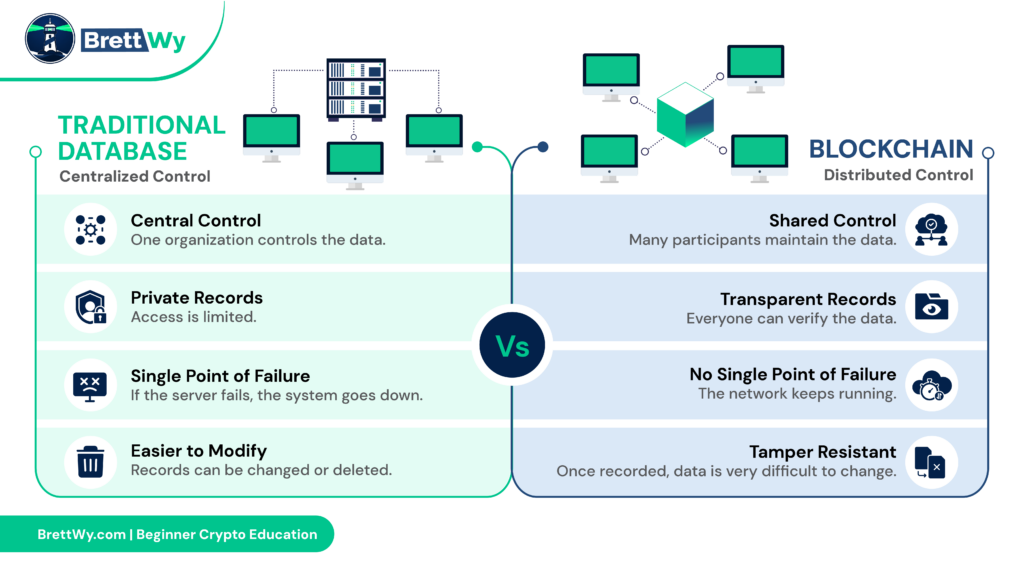

Blockchain vs Traditional Databases

Blockchain and traditional databases both store information, but they differ in ownership, control, transparency, and trust models.

| Feature | Shared Ledger | Traditional Database |

|---|---|---|

| Ownership | Distributed | Usually centralized |

| Control | Shared | One organization controls it |

| Transparency | Often public | Usually private |

| Security Model | Uses consensus | Uses access controls |

| Data Changes | Makes historical changes difficult | Allows easier edits |

| Trust Requirement | Reduces reliance on a central authority | Requires trust in the operator |

Advantages of Traditional Databases

Traditional databases are often:

- Faster

- Cheaper

- Easier to manage

Therefore, they still work better for many everyday business systems.

Advantages of Shared Ledger Systems

Shared ledger systems can offer:

- Independent verification

- Greater transparency

- Reduced single points of failure

- Tamper-resistant records

In other words, each approach serves different purposes.

What Are the Different Types of Blockchain?

Not all blockchains are public. Different models exist for different use cases.

Public Blockchains

Public networks are open to anyone.

For example, major public networks include:

- Bitcoin

- Ethereum

Anyone can:

- View records

- Participate

- Verify transactions

Private Blockchains

A specific organization controls a private network.

Therefore, access is restricted.

Companies often use these systems in enterprise environments.

Consortium Blockchains

Multiple organizations manage consortium networks together.

Because of that structure, approved participants share control.

These systems are common in industry collaborations.

What Are Smart Contracts?

Smart contracts are self-executing programs stored on a blockchain.

They automatically perform actions when predefined conditions are met.

For more detail, readers can explore Ethereum’s official documentation.

Simple Example

Imagine a digital ticket.

Once payment is received:

- Ticket ownership transfers automatically

- No manual approval is required

As a result, the program can complete the action without a middleman.

Why They Matter

Smart contracts reduce manual processes and enable decentralized applications.

They became especially popular on Ethereum.

The official Ethereum smart contracts guide provides beginner-friendly explanations of smart contracts and decentralized applications.

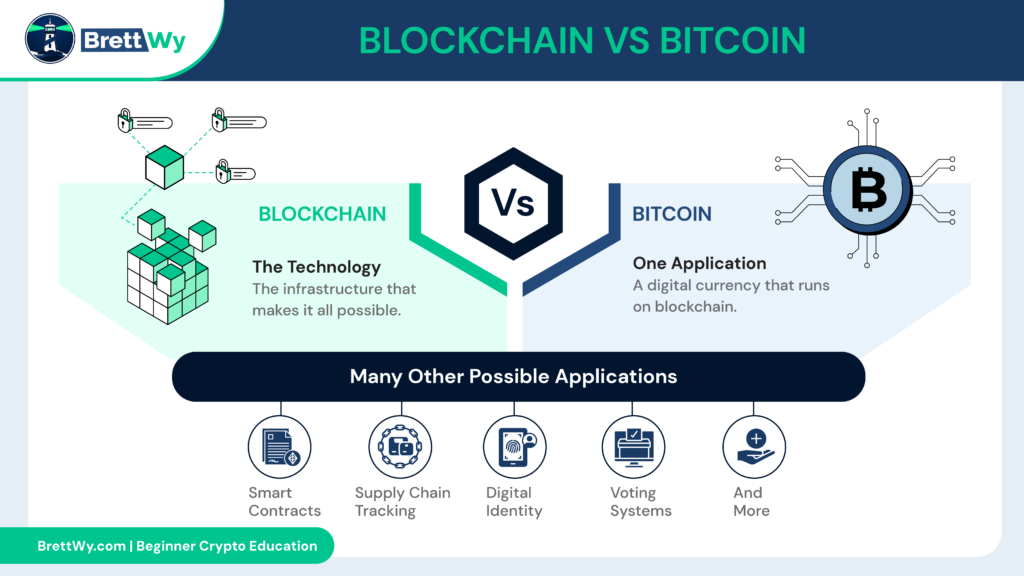

What Are Real-World Uses of Blockchain?

Blockchain is used for much more than cryptocurrency.

Because it can create shared, verifiable records, many industries explore practical uses for it.

Cryptocurrency

The most widely known use case is digital money.

For example, common crypto networks include:

- Bitcoin

- Ethereum

- Stablecoins

Supply Chain Tracking

Companies can track products as they move through production and delivery.

As a result, supply chains can become easier to audit.

Identity Verification

Shared record systems may help people prove identity while reducing fraud risks.

However, these systems still need strong privacy protections.

Voting Systems

Some researchers explore distributed ledgers for voting systems to improve auditability.

Even so, voting requires strict security, privacy, and legal safeguards.

Healthcare Records

The technology could help coordinate medical record sharing while maintaining data integrity.

However, healthcare systems must also protect sensitive personal information.

Business Applications

Businesses use distributed record systems for:

- Asset tracking

- Auditing

- Compliance

- Cross-border settlements

What Are the Advantages of Blockchain?

Blockchain offers transparency, security, accessibility, and shared verification.

Transparency

Participants can independently verify information.

Therefore, the system can reduce confusion about shared records.

Security

Cryptography and consensus mechanisms help protect records.

In addition, decentralization reduces dependence on one central system.

Reduced Intermediaries

Certain processes can operate with fewer middlemen.

However, that does not mean every middleman disappears.

Global Accessibility

Many networks operate globally and remain available around the clock.

Because of that, users in different countries can access the same network.

What Are the Limitations of Blockchain?

Blockchain offers many benefits, but it is not a perfect solution for every problem.

Scalability

Some networks process transactions more slowly than centralized systems.

As a result, fees and delays can increase during busy periods.

Energy Consumption

Certain Proof of Work systems consume significant energy.

However, Proof of Stake networks use a different design that can require much less energy.

User Responsibility

Users must protect passwords, recovery phrases, and wallet credentials.

In crypto, mistakes can be difficult to reverse.

For more beginner-focused safety guidance, read our Crypto Security Guide.

Regulation

Legal frameworks continue evolving around digital assets and distributed ledgers.

Therefore, rules can vary depending on the country, platform, and use case.

Adoption Challenges

Many applications still face usability and integration hurdles.

For beginners, this can make the technology feel harder than it needs to be.

Blockchain vs Bitcoin

Blockchain is the technology. Bitcoin is one application built using that technology.

A simple analogy:

Imagine a public road system.

The roads are the underlying technology.

The cars traveling on those roads are Bitcoin transactions.

Without roads, the cars cannot travel.

Likewise, without the ledger system, Bitcoin could not operate.

Many beginners mistakenly use the terms interchangeably.

However, Bitcoin uses blockchain technology, while the same concept has many uses beyond Bitcoin.

To continue learning, read our beginner guide to What Is Bitcoin?.

Where Beginners Get Confused About Blockchain

Beginners often get confused because blockchain is usually explained with technical language before the basic idea is clear.

“Blockchain and Bitcoin Are the Same Thing”

They are related, but they are different.

Bitcoin is a cryptocurrency.

The underlying ledger is the technology that enables Bitcoin to function.

“Blockchain Is Completely Anonymous”

Most public networks are better described as pseudonymous.

In other words, transaction histories may be public even when real names do not appear directly.

“Blockchain Cannot Be Hacked”

Individual networks may use strong security, but surrounding systems can still have weaknesses.

For example, risks can appear in:

- Exchanges

- Wallets

- Applications

- User mistakes

If you plan to use cryptocurrency, our guide to Crypto Wallets Explained is a helpful next step.

“Blockchain Solves Every Problem”

Not every database needs a distributed ledger.

Sometimes traditional systems are faster and more practical.

“Blockchain Eliminates All Trust”

This technology reduces certain trust requirements.

However, users still trust:

- Software developers

- Infrastructure providers

- Security practices

- Network rules

Key Takeaways

- Blockchain is a shared digital record-keeping system.

- Information is stored in linked blocks.

- The technology was created to help solve trust and double-spending challenges.

- Nodes maintain copies of the shared record.

- Consensus mechanisms help networks agree on valid transactions.

- Bitcoin was the first major application.

- Ethereum expanded the concept through smart contracts.

- Distributed ledgers can offer transparency and security benefits.

- However, they also have limitations and trade-offs.

- Bitcoin and the technology behind it are not the same thing.

If you are ready to continue learning, the next logical step is our guide on How To Buy Cryptocurrency.

Blockchain FAQ

What is blockchain in simple terms?

Blockchain is a shared digital record system that stores information across many computers instead of one central location.

What is a block in blockchain?

A block is a collection of verified data that gets added to the chain.

Why is blockchain important?

It enables secure, shared record keeping without requiring a single central authority.

Who invented blockchain?

Modern blockchain technology was introduced by Satoshi Nakamoto through Bitcoin in 2008.

Is blockchain the same as Bitcoin?

No. Blockchain is the technology. Bitcoin is a cryptocurrency that uses it.

Can blockchain be hacked?

Major networks are designed to be highly secure. However, related systems such as exchanges and wallets can still be compromised.

What are nodes?

Nodes are computers that participate in maintaining and verifying shared records.

What is decentralization?

Decentralization means control is distributed among many participants rather than one central organization.

What is Proof of Work?

Proof of Work is a consensus mechanism used by Bitcoin that relies on miners validating transactions.

What is Proof of Stake?

Proof of Stake is a consensus mechanism that relies on validators rather than mining competition.

What are smart contracts?

Smart contracts are self-executing programs stored on a distributed ledger. They automatically perform actions when conditions are met.

Is blockchain only used for cryptocurrency?

No. Blockchain also has applications in supply chains, identity systems, healthcare, auditing, and more.

Final Definition

Blockchain is a decentralized digital record-keeping system that stores information in linked blocks across a network of computers. It enables secure, transparent, and verifiable record keeping without relying on a single central authority. As a result, it serves as the foundational technology behind Bitcoin, Ethereum, and many other digital applications.